Pendle 2024 Year in Review and Future Outlook

Article Source: Pendle

Foreword

The Pendle team was founded in mid-2020, as we were exploring how to introduce fixed interest rates into the DeFi frenzy of crazy Annual Percentage Yields (APY). Five years in the crypto world can feel like an eternity, yet the time has passed in the blink of an eye.

I am proud of the team's achievements to date and the challenges we have overcome. We are poised to continue our growth trajectory. As the industry evolves, leveraging years of expertise and experience, we are uniquely positioned to capture new opportunities.

This article will outline the following:

· 2024 Pendle Milestones

· Pendle's Three Pillars

· V2 Upgrade

· Building the "Fortress"

· Boros New Project

· Endgame Vision

Pendle V2 2024 Highlights

Establishing the Fixed Income Market

2024 is a milestone year for Pendle. We have validated the market's strong demand for fixed income and demonstrated the protocol's ability to scale from millions to billions.

In early 2023, our Total Value Locked (TVL) was $230 million, soaring to $4.4 billion by the end of 2024, a 20x increase. The trading volume growth is even more astounding—average daily volume leaped from $1.1 million in 2023 to $96.4 million in 2024, nearly a 100x surge. With increased user trust in the protocol, users holding over $100 million in PT positions have become increasingly common.

On June 26, 2024, we successfully completed the largest-ever expired position settlement: Pendle seamlessly settled $3.8 billion worth of expired positions in a matter of days.

Measuring by TVL, Pendle's scale is now comparable to the fifth-largest blockchain, trailing only Ethereum, Solana, Tron, and BNB Chain.

Pendle has proven its worth.

Today, Pendle's TVL and trading volume have placed it among the ranks of DeFi blue-chip protocols. We hold over half of the share in DefiLlama's "yield-bearing" protocols.

By 2024, we can confidently state that Pendle has not only established yield trading as a separate track but has also made it one of the largest sectors in the DeFi ecosystem.

DeFi Engine

By 2024, Pendle has launched nearly 200 multi-asset, multi-term liquidity pools on 5 different chains, averaging 4 new markets added per week. By the peak in December 2024, we are concurrently operating 121 active markets, a 2.5x increase from the previous year.

But this is not just a victory of scale. These markets have become a central hub for other projects to build deep liquidity.

Today, Pendle has become the launch engine for emerging tracks and protocols.

It has been proven that Pendle is not only a liquidity hub for protocols but also a cornerstone of growth for the entire DeFi ecosystem. At its peak, 48% of Ethena's TVL came from Pendle; for every 100 BTCs re-staked in the BTCfi ecosystem, 42 were deposited through Pendle; and Usual's scale surged from $3 billion to a peak of $12 billion, with around 30% of the growth contributed by Pendle.

The beneficiaries are not only the protocols—ecosystems like Arbitrum, Zircuit, Berachain have significantly boosted liquidity through Pendle.

Pendle's PT (Principal Tokens) itself has evolved into a $12 billion secondary economy, representing 3.3% of the total collateral in the EVM on-chain lending market. Approximately 20% of Morpho's platform deposits come from Pendle.

Where there's yield, there's Pendle.

Over the past year, we have made a significant leap forward, turning Pendle into a premier yield trading platform. But the mission is far from over—the journey continues.

Three Pillars of Global Expansion

V2 Upgrade

The on-chain annual yield market is approximately $17.7 billion, with only 4.97% ($880 million) of the yield made tradeable through Pendle (i.e., "Pendled"). Pendle has established its presence, but the market is still expanding, with untapped yield potential far exceeding our current coverage.

We are still far from our goal of "controlling the yield layer," but the journey has begun.

The V2 upgrade will help us bridge the gap through the following fundamental improvements:

1. Open Ecosystem

The protocol is inherently permissionless. Several third-party protocols have previously deployed pools on Pendle through external development. We will open this feature through the UI, enabling more participants to leverage Pendle's technology to autonomously create yield markets. This dual-track strategy—growth achieved through community-driven permissionless listings, complemented by strategic curation from the business team—will drive Pendle's scalable expansion.

2. Dynamic Fees

Fee optimization is a future focus aimed at balancing the long-term interests of liquidity providers (LPs), users, and the protocol. We will implement a dynamic fee-rebalancing mechanism to ensure that the pools remain in optimal condition amidst interest rate fluctuations.

3. vePENDLE Enhancements

The functionality of vePENDLE will extend beyond weekly on-chain voting, opening participation channels to all users (regardless of scale). Optimizing the protocol interaction process for vePENDLE holders will also be a core focus across all business lines (more details below).

Currently, the V2 version has been battle-tested and will continue to serve as Pendle's core weapon in tackling the DeFi yield market. Building on our existing achievements, we will drive product expansion this year with a more aggressive and expansive strategy.

Thus, we move towards the next vertical—building "Citadels" as strategic outposts for the new generation of users.

Building the "Stronghold"

By 2024, Pendle had reached a billion-dollar scale. Today, our goal is in the trillion-dollar range.

Currently, Pendle only serves DeFi users within the EVM ecosystem. Despite the EVM market being vast and performing well, we believe Pendle should not be limited to this. The "Stronghold" plan aims to break through this boundary.

Where there is yield, there is Pendle.

Our goal is for Pendle to be at the core of the user experience, no matter how users interact with the DeFi yield layer.

Currently, Pendle V2 covers only about 5% of the DeFi yield market but has already become one of the largest protocols. The size of the interest rate derivatives market is as high as $558 trillion—30,000 times the current yield market. If the "Stronghold" can capture even a tiny share of it, Pendle will achieve exponential growth.

We are exploring and advancing three "Stronghold" plans:

1. Expansion of PT to Non-EVM Ecosystems

The first Stronghold outpost will drive PT (Principal Token) expansion to ecosystems beyond the EVM.

Non-EVM chains like Solana, TON, HYPE, and others experienced explosive growth last year, attracting millions of potential users. By providing a one-click fixed income gateway to cover these ecosystems, Pendle will quickly capture untapped opportunities and usher in a wave of new users.

2. TradFi Placement for PT

The second Stronghold will focus on compliant products, packaging yield for regulatory bodies, establishing distribution channels to enable traditional financial institutions to access the best crypto-native fixed income.

We will collaborate with partners like Ethena to launch a Special Purpose Vehicle (SPV) managed by a compliant asset management institution, opening up Pendle access to traditional financial clients.

3. Shariah-Compliant PT for Islamic Funds

Similarly, Pendle will also create a stronghold that complies with Shariah principles. Islamic finance is a global market worth $3.9 trillion, spanning over 80 countries. Over the past decade, Shariah-compliant financial products have experienced explosive growth at an annual rate of 10%.

New Project Boros

The Power to Disrupt Reality

As builders navigating through multiple cycles, we understand well the industry's dynamics—memetic shifts and protocol developments always wax and wane. Yet, blockchain technology sees new highs with each cycle, presenting an optimal moment to break through technological boundaries.

Pendle firmly believes that the most transformative blockchain applications should be able to efficiently address real-world issues more effectively than traditional finance—especially in markets plagued by illiquidity, low transparency, and closed systems.

Our envisioned Boros is precisely such an application: leveraging blockchain technology to achieve functionalities that traditional finance could not reach.

Anchoring the Greatest Yield Source

As the ultimate yield platform, we have witnessed the surge in demand for yield trading firsthand. Pendle V2's yield markets have demonstrated significant growth potential, fueled by the market's widespread demand for yield hedging and speculation.

Boros will take this vision to new heights. It can support any type of yield—whether in DeFi, CeFi, or traditional financial markets like LIBOR rates or mortgage rates—significantly expanding Pendle's market coverage and reshaping the possibilities in the yield space.

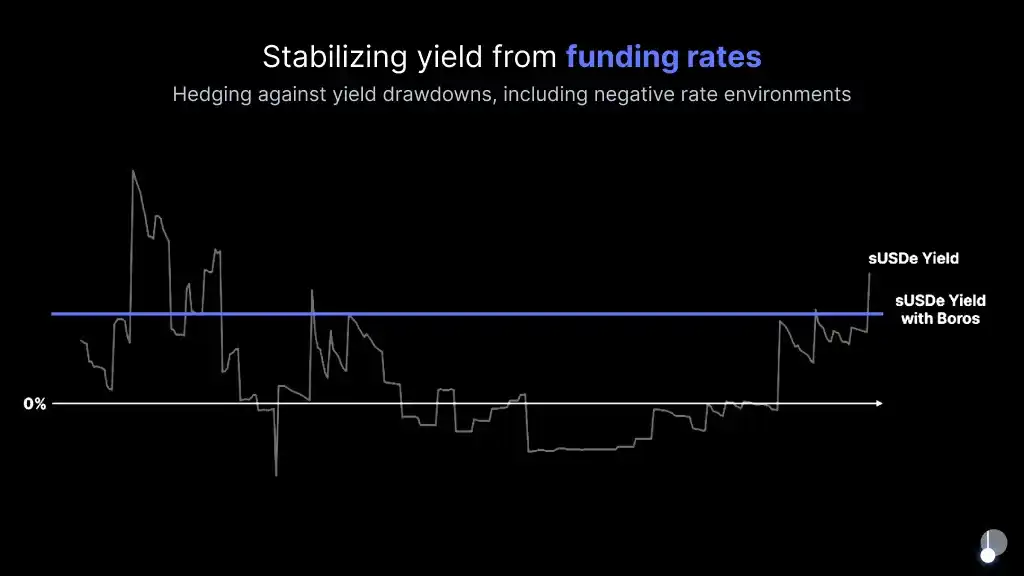

Boros's primary target is the crypto market's greatest yield source—the funding rate.

The perpetual contract market sees an average daily open interest of $150 billion, with the funding rate flowing every second in the ever-active market; the daily trading volume reaches $200 billion, surpassing the spot market by 10 times. The yield potential here is significant enough to overshadow V2's current spot market.

Through Boros, Ethena can achieve absolute control and predictive ability over yield, locking in a fixed funding rate to ensure the stability of large-scale operations.

Boros swaps the floating yield stream of underlying assets for a fixed yield stream (and vice versa) until maturity, enabling rate trading

Another classic case is the TRUMP contract launched on a perpetual DEX—long position holders face funding rates as high as 20,000% APY, severely eroding short-term profits. Boros offers a new solution: TRUMP/USDT perpetual traders can hedge to convert the variable funding rate into a fixed payment.

Conversely, traders executing the flash loan arbitrage strategy can also capture high-yield opportunities and secure fixed returns.

Boros, by providing robust yield control and optimization tools, establishes a new standard for funding rate interactions.

How Does PENDLE Fit into This Vision?

Where there's yield, there's Pendle.

As the ecosystem expands, the value created by the protocol through the three pillars of V2, the Citadel, and Boros will materialize as yield flowing to vePENDLE.

By 2024, active vePENDLE holders will be the primary beneficiaries of Pendle's growth—enjoying an average annualized yield of around 40%, not including the $6.1 million airdrop value distributed in December.

Endgame Vision

From Pendle's inception, the vision has been clear: to become a top-tier yield trading protocol. While this goal remains unchanged, our mission has evolved in tandem with the growth of our business.

Pendle is committed to being the ultimate gateway for user yield interactions.

Whether it's a crypto-native enthusiast or a Middle Eastern sovereign wealth fund, Pendle will serve as the entry point for various forms of yield interactions. From DeFi to CeFi, we provide protocols, interfaces, and tools to empower the complete yield journey.

The 2025 roadmap entails bold innovations, with the Citadel and Boros emerging as two new verticals. We understand that not all plans can be executed flawlessly. When faced with obstacles, we will adjust our strategies, reassess, and chart new paths forward—just as we have done over the past few years.

Amidst the market turmoil of 2025, rife with disruption and panic, we will anchor ourselves to our mission: expand V2, drive PT distribution to new heights, and unleash the potential of Boros. Instead of competing on others' tracks, we will focus on our established goals and march forward with determination.

Looking ahead and overcoming current challenges, we firmly believe that Pendle is steadily progressing towards its goal of the “Unified Yield Layer.”

The mission is not yet complete, but it will be accomplished. (Job is not done—but it will be.)

TN

Pendle CEO and Co-Founder

This article is a contribution and does not represent the views of BlockBeats.

You may also like

Why Is BlackRock Investing $5 Billion in the SpaceX IPO?

Cryptocurrency market makers collectively seek change as it becomes increasingly difficult to make money

a16z Crypto Partner: Cash flow is the moat

Citibank releases "2030 Asset Tokenization Market Outlook": 6 major trends may create a $8.2 trillion market

The trillion-dollar valuation test: Are the three major super IPOs a celebration for tech stocks or a nightmare for the crypto market?

Morning Report | Digital Asset completes $355 million financing led by a16z Crypto; Meta completes operational separation from Manus

Morning News | CME Group launches Nasdaq Cryptocurrency Index futures; Asset management giant Janus Henderson strategically invests in Ethena

Bitcoin Layer 2 Network Botanix: Why Did We Choose to Dissolve?

Why did Oracle deliver the strongest financial report in history, yet its stock price fell?

When the P2P illicit funds from ten years ago turned into 60,000 bitcoins

Dialogue with OmenX Founder: Why does the prediction market need an evolution from "spot" to "derivatives"?

Galaxy in-depth report: Is Solana still worth paying attention to?

Young people in South Korea make a "final effort" in the epic bull market

The pricing controversy of Trade.xyz exposes the fatal weakness of Pre-IPO perpetual contracts

How much longer can Ethereum's last big buyer hold on?

World Cup 2026 Coming – WEEX Celebrates with $1M Prize Pool & Michael Owen Live

Morning Report | OpenAI has submitted an S-1 registration statement draft to the U.S. SEC; Morpho completes $175 million financing